Michael Burry, also known as 'big short,' is a former hedge fund manager who has made legendary bearish calls over the last few decades.

Burry foresaw the subprime mortgage crisis of 2007 and made close to a billion dollars for his investors by taking short positions on the mortgage bond market.

Since then, he has come out swinging at several of Wall Street's darlings and recently suggested that the US equity market is in the process of a catastrophic correction.

In filings released in August last year, it was revealed Burry sold off all of his long equity positions except one, dumping millions of shares in the process. Companies he abandoned ranged from those in the FAANG acronym, such as Alphabet (NASDAQ GOOGL), and Meta Platforms (NASDAQ: META) to financial services firms Cigna Corp (NYSE: CI) and travel technology companies Booking Holdings (NASDAQ: BKNG).

Perhaps ominously, the only share remaining in his portfolio is The GEO Group Inc (NYSE: GEO), which operates a network of private prisons and secure mental health units worldwide.

The indiscriminate sell-off in Burry's portfolio also backs up his opinion that the US is already in a recession and that a vast value transfer from bulls to bears is unfolding.

Take a deeper look at Burry's thesis for where the stock market is heading.

S&P 500 makes a correction

Burry believes the S&P 500 has passed a downside inflection point, which looks to have been sometime in January 2020. This is when a downtrend officially began per the 10-week Supertrend indicator, and the index then moved below the 50-week simple moving average (SMA) shortly after.

A frightening convergence of the 50-week and 200-week SMAs may help to confirm Burry's thesis that we're on the way to the bottom. Judging by the short (and closing) distance between the indicators, downside stock momentum, and directional trend, it looks more than likely these moving averages will soon cross over.

If this happens, it will create one of the most psychologically powerful and statistically significant sell signals respected by Wall Street traders, aptly named the death cross. A death cross pattern in the S&P 500 has foreshadowed many catastrophes in financial markets, including the global financial crisis and the announcement of the COVID-19 pandemic.

When one considers that the S&P 500 had been on one of the largest bull runs in history, lasting over nine years, and that the index traded at overbought or nearly overbought levels for much of it, and that we saw rapid changes to our civilization in the last three years, combined with economic and political trauma and the pessimistic expectation that the worst is yet to come, this idea starts hitting home for many.

A Superbubble explosion

A complimentary idea that could explain the 'why?' in Burry's thesis can be found in an article published by legendary investor Jeremy Grantham in August last year named "entering the superbubble's final act."

Grantham is also a prolific stock market bear, having successfully predicted the dot-com bubble in the 90s and correctly foresaw the arrival of the subprime mortgage crisis in 2007 along with Burry.

As co-founder and chief investment strategist of hedgefund Mayo, & van Otterloo, Grantham described stocks, bonds, housing, and commodities as being in an overpriced 'superbubble'. These economic cycles were said to have caused immense damage to economies in the past, and today's superbubble was said to share characteristics with three others from recent history.

The similarities included overvaluation and an overconfident bear market rally that poured gasoline on the fire to accelerate their explosions.

Lighting the match is a breakdown in the economy's fundamentals, which could be in the process of unfolding before our eyes.

"If history repeats, the play will once again be a Tragedy. We must hope this time for a minor one," wrote Grantham.

Cracks begin to show

Besides the ongoing threats of inflation eating up people's income, the continued rise of interest rates, mounting geopolitical instabilities, and all the other problems carried over from the pandemic, other threats are emerging that have historically been the leading indicators of a recession.

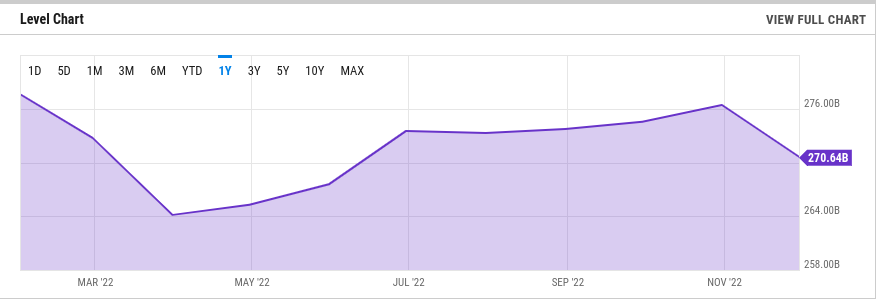

Durable goods new orders in the US are down 2.09% from last month to $270.64 billion and up from $270.07 billion last year. If this is a sign of a new trend kicking off, manufacturers and other businesses think the economy will slow down due to spending less on capital expenditures.

We may have a better idea of this when the results are posted for December.

Then there's the International Monetary Fund (IMF) sounding the alarm that a third of the world will be in a recession this year and that Europe, the Americas, and leading developing economies such as China will all enter a recession simultaneously, which is something unheard of in the last 40 years.

This makes China's economic recovery all the more pivotal to the world stage, as it also props up other export-heavy economies that depend on it for buying goods for internal consumption. The country's GDP figures are expected to be confirmed tomorrow, and expectations are that it will show a severely maimed China still coming to grips with large outbreaks of COVID-19.

Balancing the Jenga pieces for China is its reliance on its real estate market, which is often a massively underappreciated factor when coming to grips with its economic recovery despite a boom expected in consumer spending. About $1.41 trillion dollars or around 18-30% of China's GDP is tied up in real estate, which can be explained by the fact that most investors use it as a vehicle for speculation and that only new real estate developments are seen as desirable investments.

House prices in China shrank 1.5% in December, recording a seventh-straight month of losses. A liquidity squeeze is still on the cards as extremely overleveraged banks and developers still pose a credit risk to investors of being unable to withdraw their savings or redeem bond coupons or principals.

It's yet to be seen if the leading indicator of a recession, namely the negative wealth effect, will gain momentum in China as the real estate market continues to make lower lows and lower highs. People seeing their net worth dry up via a fall in house values may also price them out of getting credit for daily living, thus reducing household consumption and kicking off a recessionary tailspin, as has been commonly observed in developed countries such as the United States.