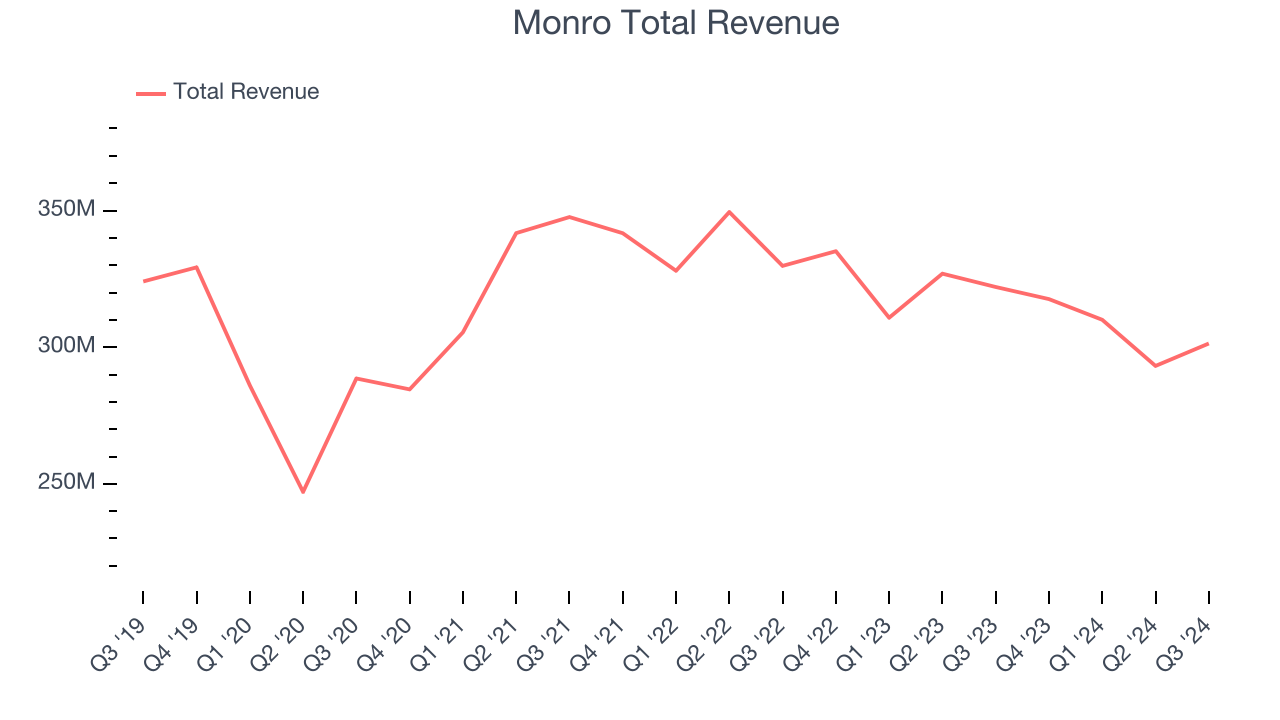

Auto services provider Monro (NASDAQ:MNRO) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 6.4% year on year to $301.4 million. Its non-GAAP profit of $0.17 per share was 34.6% below analysts’ consensus estimates.

Is now the time to buy Monro? Find out by accessing our full research report, it’s free.

Monro (MNRO) Q3 CY2024 Highlights:

- Revenue: $301.4 million vs analyst estimates of $300.1 million (in line)

- Adjusted EPS: $0.17 vs analyst expectations of $0.26 (34.6% miss)

- Gross Margin (GAAP): 35.3%, in line with the same quarter last year

- Operating Margin: 4.4%, down from 6.9% in the same quarter last year

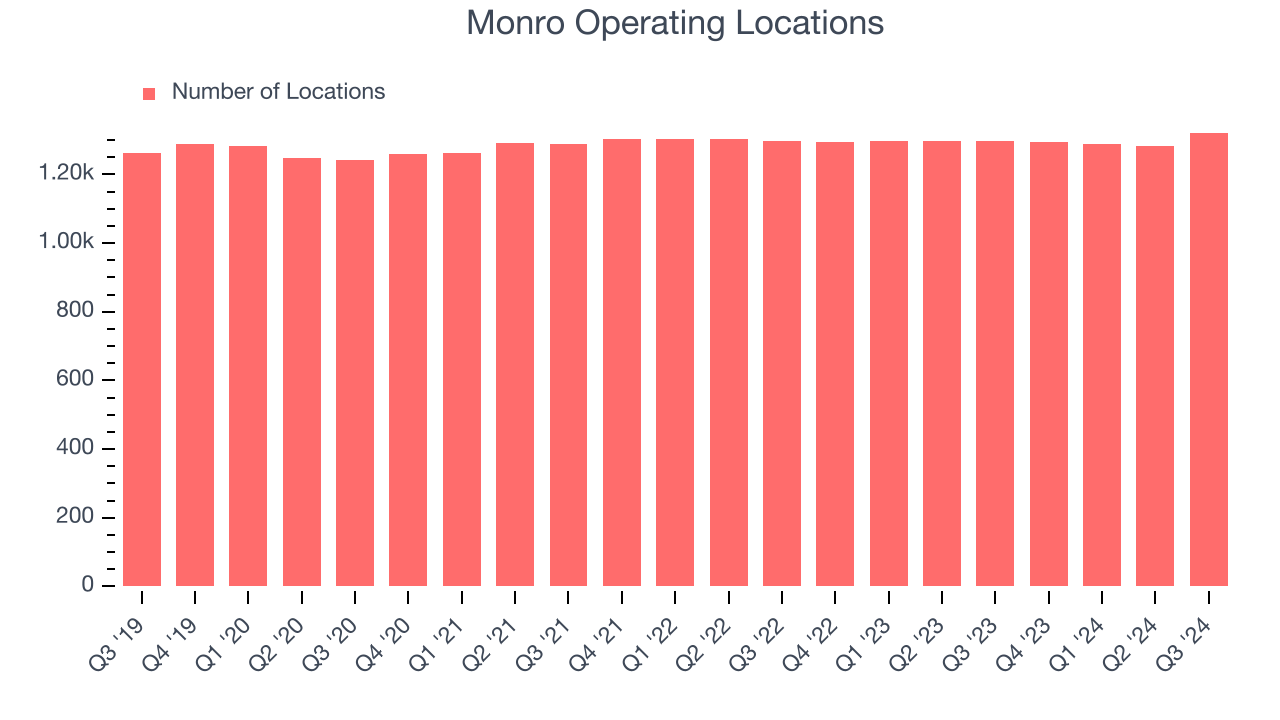

- Locations: 1,322 at quarter end, up from 1,298 in the same quarter last year

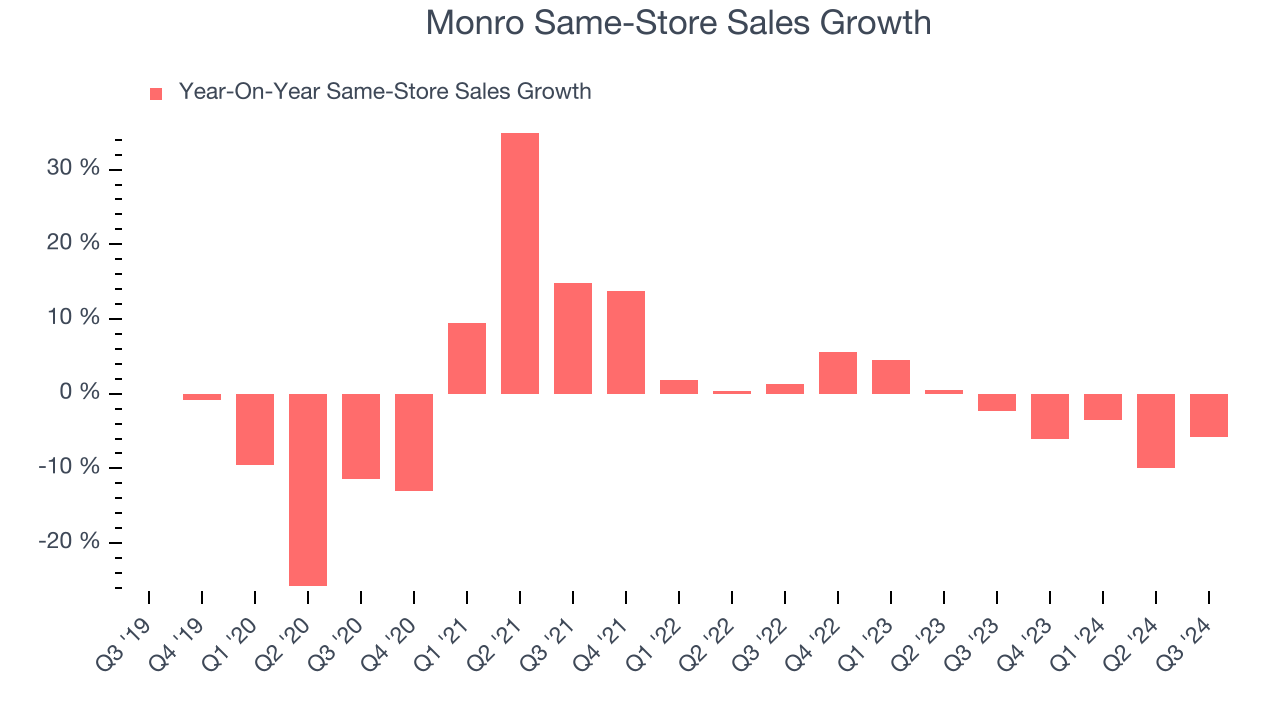

- Same-Store Sales fell 5.8% year on year (-2.3% in the same quarter last year)

- Market Capitalization: $801.6 million

“We drove sequential improvement in our year-over-year comparable store sales percentage change from the first quarter as well as a significant acceleration in our comp trends as the second quarter progressed. Importantly, our tire dollar and unit sales improved sequentially from the first quarter and our tire category exited the quarter with year-over-year growth in units in the month of September. Our ConfiDrive digital courtesy inspection process and our oil change offer allowed us to drive sequential improvement from the first quarter in our service category sales as well as year-over-year growth in both battery units and sales dollars in the quarter. Additionally, we improved our attachment rate for alignments, which resulted in year-over-year growth in both alignment units and sales dollars in the month of September. Encouragingly, our sales momentum from the second quarter has continued into fiscal October with our preliminary comparable store sales down only 1%, supported by improving trends in tires and all service categories, including brakes. Excluding the impact of Hurricanes Helene and Milton, our preliminary comparable store sales would have been approximately flat compared to the prior year”, said Mike Broderick, President and Chief Executive Officer.

Company Overview

Started as a single location in Rochester, New York, Monro (NASDAQ:MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years.

Monro is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, Monro’s demand was weak over the last five years (we compare to 2019 to normalize for COVID-19 impacts). Its sales were flat because it didn’t open many new stores and observed lower sales at existing, established locations.

This quarter, Monro reported a rather uninspiring 6.4% year-on-year revenue decline to $301.4 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and indicates the market believes its newer products will not lead to better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Monro listed 1,322 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth for shops open for at least a year.

Monro’s demand has been shrinking over the last two years as its same-store sales have averaged 2.1% annual declines. This performance isn’t ideal, and we’d be concerned if Monro starts opening new stores to artifically boost revenue growth.

In the latest quarter, Monro’s same-store sales fell by 5.8% annually. This decrease was a further deceleration from the 2.3% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Monro’s Q3 Results

It was encouraging to see Monro narrowly top analysts’ revenue expectations this quarter. On the other hand, its gross margin missed analysts’ expectations and its EPS missed Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.7% to $25.79 immediately after reporting.

Monro may have had a tough quarter, but does that actually create an opportunity to invest right now?We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.