Lifting and material handling equipment company Terex (NYSE:TEX) reported Q3 CY2024 results exceeding the market’s revenue expectations, but sales fell 6.1% year on year to $1.21 billion. The company’s full-year revenue guidance of $5.1 billion at the midpoint also came in 2.4% above analysts’ estimates. Its non-GAAP profit of $1.46 per share was also 15.7% above analysts’ consensus estimates.

Is now the time to buy Terex? Find out by accessing our full research report, it’s free.

Terex (TEX) Q3 CY2024 Highlights:

- Revenue: $1.21 billion vs analyst estimates of $1.16 billion (4.2% beat)

- Adjusted EPS: $1.46 vs analyst estimates of $1.26 (15.7% beat)

- EBITDA: $141 million vs analyst estimates of $136.8 million (3% beat)

- EBITDA guidance for the full year is $652.5 million at the midpoint, above analyst estimates of $639.6 million

- Gross Margin (GAAP): 20.2%, down from 22.7% in the same quarter last year

- Operating Margin: 10.1%, down from 12.7% in the same quarter last year

- EBITDA Margin: 11.6%, down from 13.6% in the same quarter last year

- Free Cash Flow Margin: 7.2%, down from 8.2% in the same quarter last year

- Market Capitalization: $3.63 billion

Company Overview

With humble beginnings as a dump truck company, Terex (NYSE:TEX) today manufactures lifting and material handling equipment designed to move and hoist heavy goods and materials.

Construction Machinery

Automation that increases efficiencies and connected equipment that collects analyzable data have been trending, creating new sales opportunities for construction machinery companies. On the other hand, construction machinery companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the commercial and residential construction that drives demand for these companies’ offerings.

Sales Growth

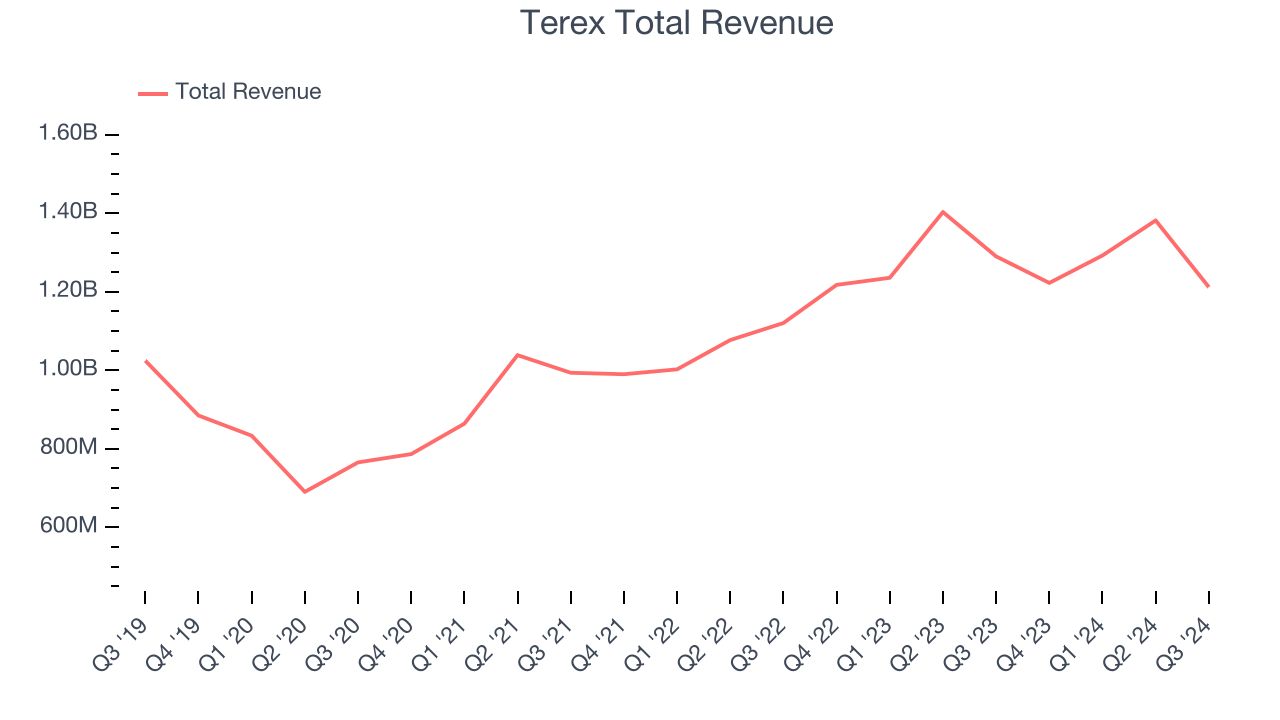

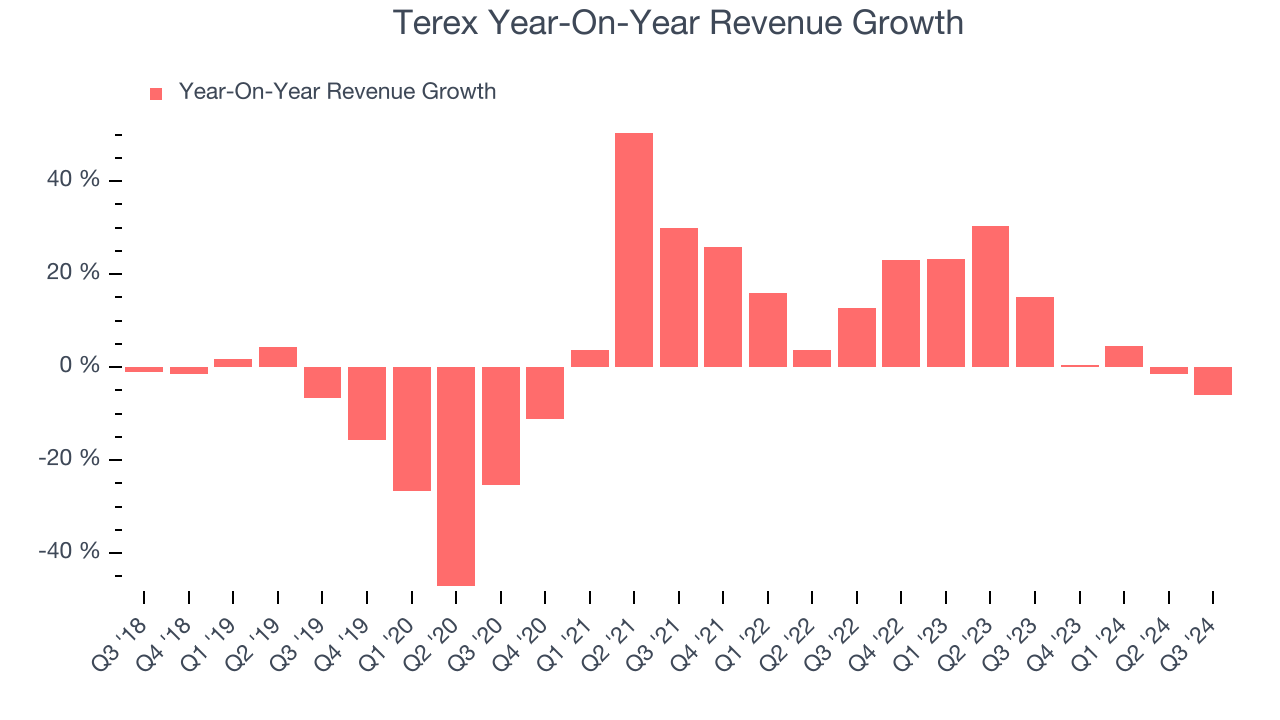

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Terex’s sales grew at a sluggish 2.5% compounded annual growth rate over the last five years. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Terex’s annualized revenue growth of 10.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Terex’s revenue fell 6.1% year on year to $1.21 billion but beat Wall Street’s estimates by 4.2%.

Looking ahead, sell-side analysts expect revenue to decline 2.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates the market believes its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

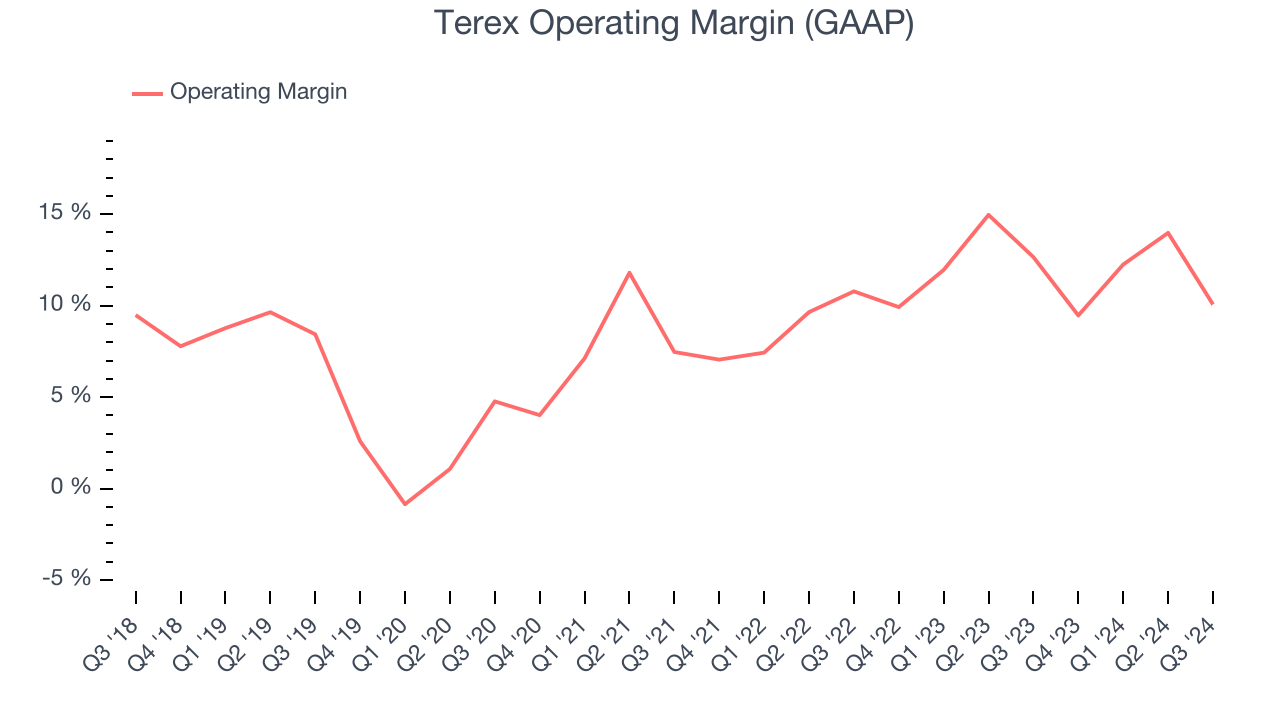

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Terex has done a decent job managing its cost base over the last five years. The company produced an average operating margin of 9.1%, higher than the broader industrials sector.

Looking at the trend in its profitability, Terex’s annual operating margin rose by 9.7 percentage points over the last five years, showing its efficiency has meaningfully improved.

This quarter, Terex generated an operating profit margin of 10.1%, down 2.6 percentage points year on year. Since Terex’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

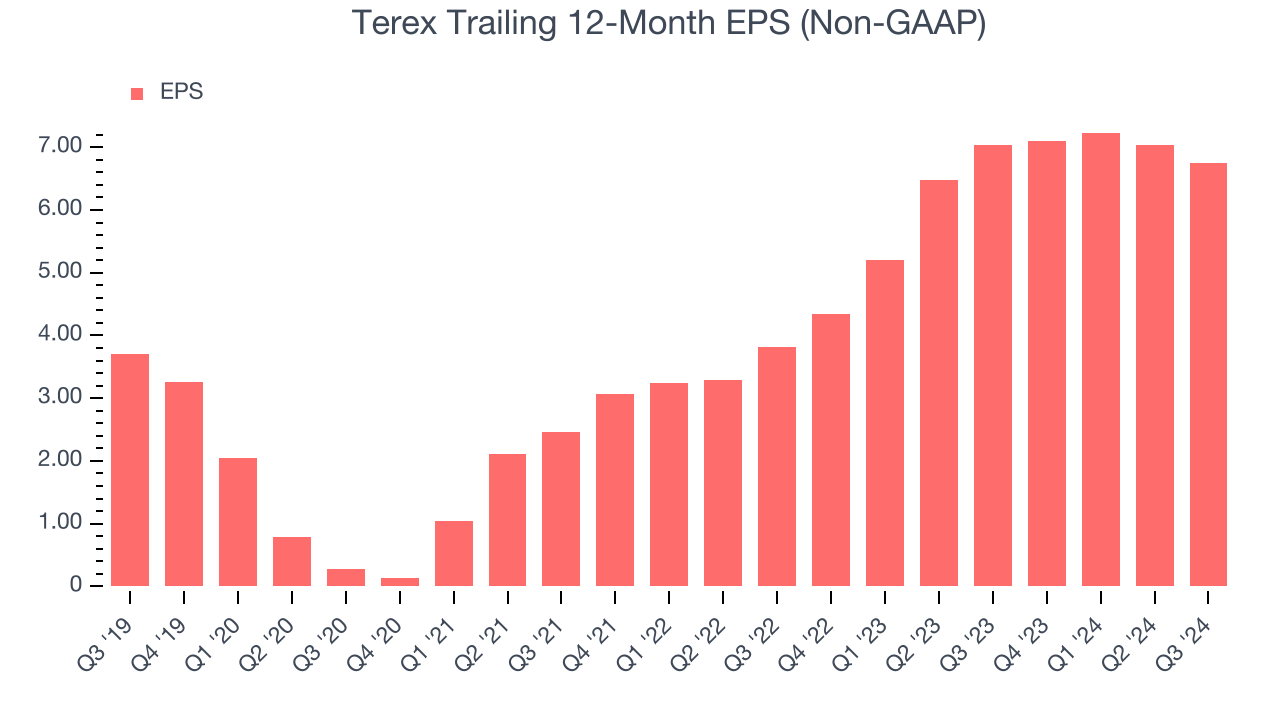

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Terex’s EPS grew at a remarkable 12.8% compounded annual growth rate over the last five years, higher than its 2.5% annualized revenue growth. This tells us the company became more profitable as it expanded.

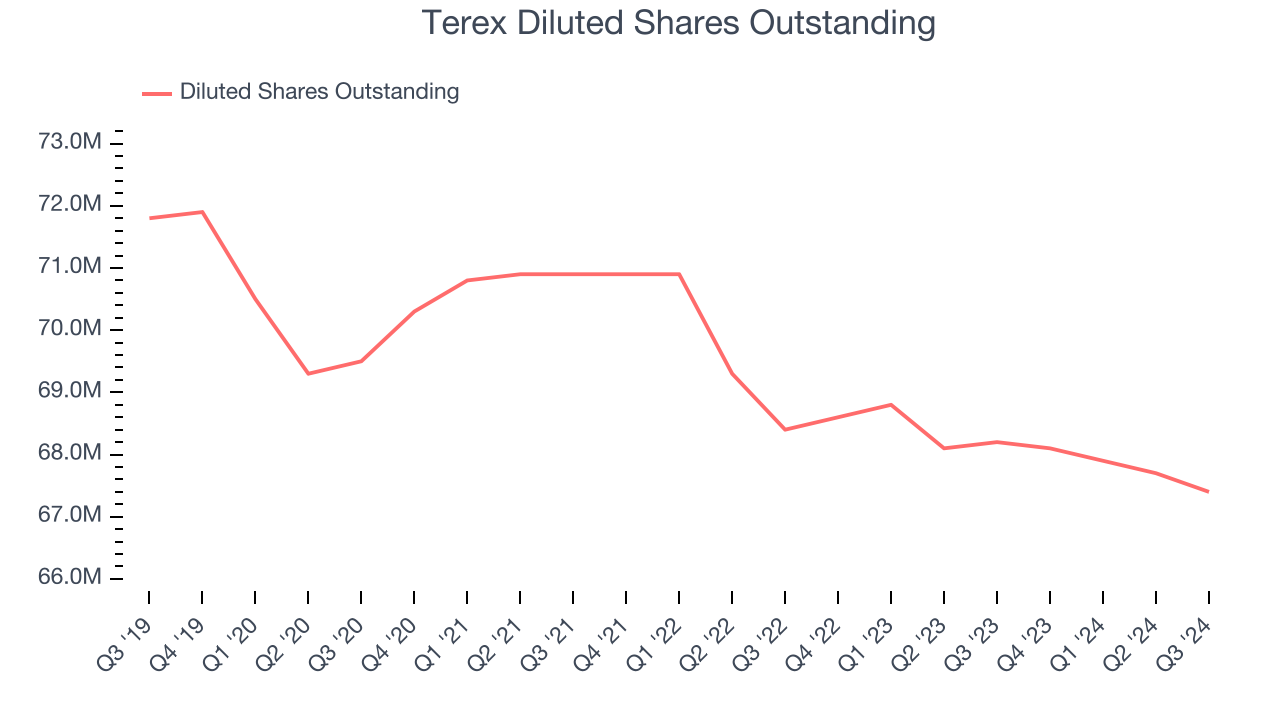

Diving into the nuances of Terex’s earnings can give us a better understanding of its performance. As we mentioned earlier, Terex’s operating margin declined this quarter but expanded by 9.7 percentage points over the last five years. Its share count also shrank by 6.1%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

For Terex, its two-year annual EPS growth of 32.9% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.In Q3, Terex reported EPS at $1.46, down from $1.75 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Terex’s full-year EPS of $6.74 to shrink by 21.9%.

Key Takeaways from Terex’s Q3 Results

We liked that Terex beat analysts’ revenue and EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance came in higher than Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 3.4% to $56.10 immediately after reporting.

Terex may have had a good quarter, but does that mean you should invest right now?The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.