Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at Vishay Intertechnology (NYSE:VSH) and its peers.

Demand for analog chips is generally linked to the overall level of economic growth, as analog chips serve as the building blocks of most electronic goods and equipment. Unlike digital chip designers, analog chip makers tend to produce the majority of their own chips, as analog chip production does not require expensive leading edge nodes. Less dependent on major secular growth drivers, analog product cycles are much longer, often 5-7 years.

The 15 analog semiconductors stocks we track reported a mixed Q3. As a group, revenues beat analysts’ consensus estimates by 0.8% while next quarter’s revenue guidance was 3.2% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.3% since the latest earnings results.

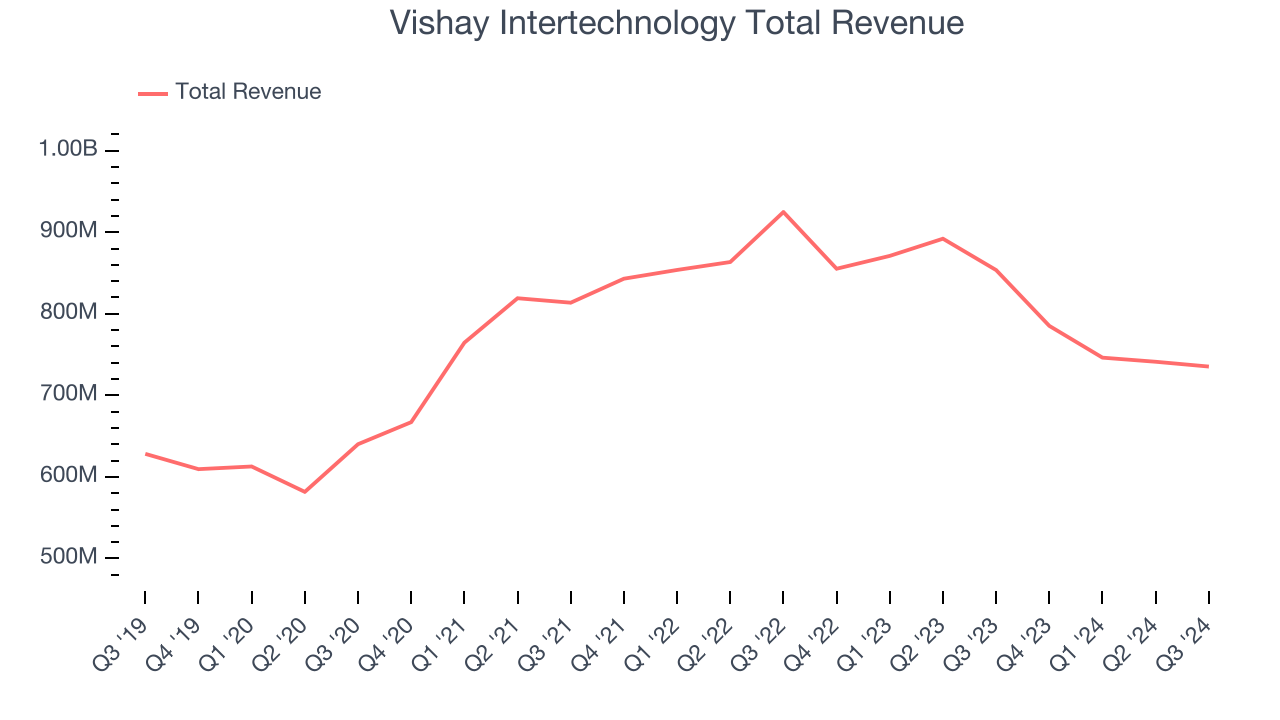

Slowest Q3: Vishay Intertechnology (NYSE:VSH)

Named after the founder's ancestral village in present-day Lithuania, Vishay Intertechnology (NYSE:VSH) manufactures simple chips and electronic components that are building blocks of virtually all types of electronic devices.

Vishay Intertechnology reported revenues of $735.4 million, down 13.9% year on year. This print fell short of analysts’ expectations by 1.8%. Overall, it was a disappointing quarter for the company with full-year revenue guidance missing analysts’ expectations.

“For the third consecutive quarter this year, revenue has held fairly constant, reflecting a prolonged period of inventory de-stocking as the pace of consumption by industrial customers remains slow, backlogs are pushed out and macroeconomic conditions in Europe worsen,” said Joel Smejkal, President and CEO.

Vishay Intertechnology delivered the weakest full-year guidance update of the whole group. Interestingly, the stock is up 12.7% since reporting and currently trades at $19.22.

Read our full report on Vishay Intertechnology here, it’s free.

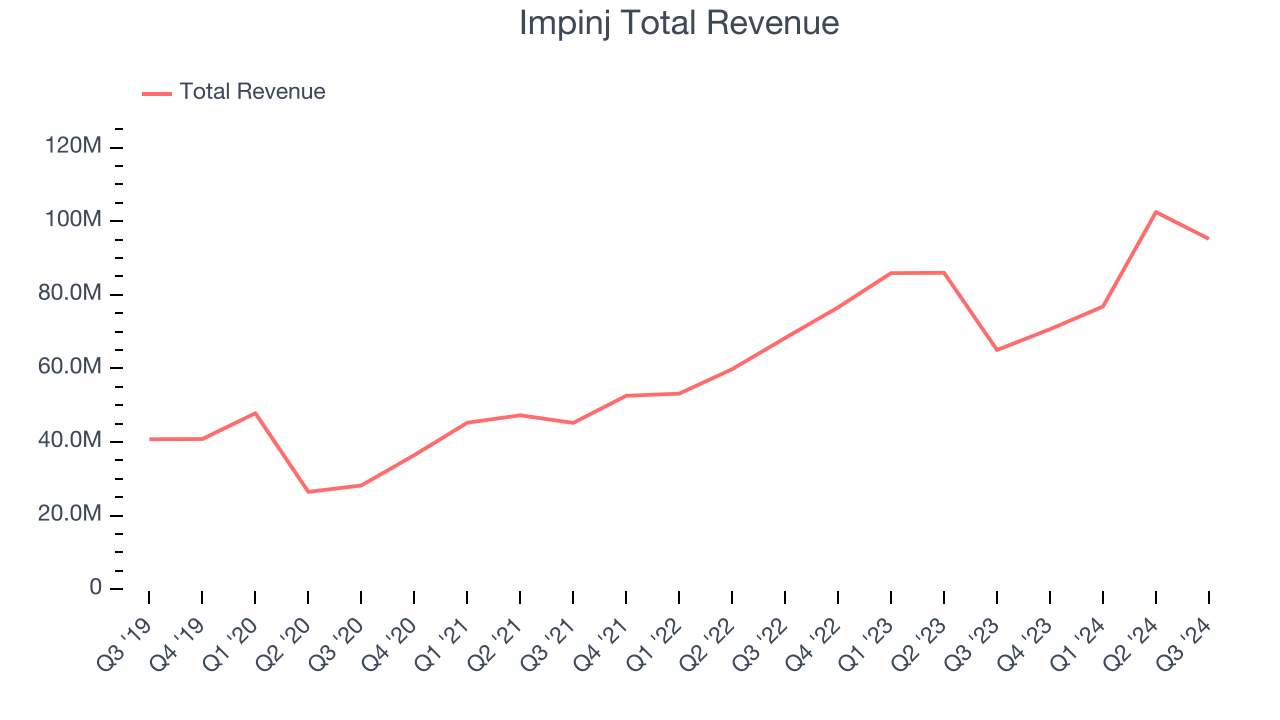

Best Q3: Impinj (NASDAQ:PI)

Founded by Caltech professor Carver Mead and one of his students Chris Diorio, Impinj (NASDAQ:PI) is a maker of radio-frequency identification (RFID) hardware and software.

Impinj reported revenues of $95.2 million, up 46.4% year on year, outperforming analysts’ expectations by 2.5%. The business had a very strong quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ adjusted operating income estimates.

Impinj pulled off the fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 13.6% since reporting. It currently trades at $191.

Is now the time to buy Impinj? Access our full analysis of the earnings results here, it’s free.

Sensata Technologies (NYSE:ST)

Originally a temperature sensor control maker and a subsidiary of Texas Instruments for 60 years, Sensata Technology Holdings (NYSE: ST) is a leading supplier of analog sensors used in industrial and transportation applications, best known for its dominant position in the tire pressure monitoring systems in cars.

Sensata Technologies reported revenues of $982.8 million, down 1.8% year on year, falling short of analysts’ expectations by 0.5%. It was a slower quarter as it posted revenue guidance for next quarter missing analysts’ expectations.

As expected, the stock is down 5.7% since the results and currently trades at $31.73.

Read our full analysis of Sensata Technologies’s results here.

Himax (NASDAQ:HIMX)

Taiwan-based Himax Technologies (NASDAQ:HIMX) is a leading manufacturer of display driver chips and timing controllers used in TVs, laptops, and mobile phones.

Himax reported revenues of $222.4 million, down 6.8% year on year. This number beat analysts’ expectations by 1.1%. It was a very strong quarter as it also produced an impressive beat of analysts’ EPS estimates and an improvement in its inventory levels.

The stock is up 1.3% since reporting and currently trades at $6.03.

Read our full, actionable report on Himax here, it’s free.

Power Integrations (NASDAQ:POWI)

A leading supplier of parts for electronics such as home appliances, Power Integrations (NASDAQ:POWI) is a semiconductor designer and developer specializing in products used for high-voltage power conversion.

Power Integrations reported revenues of $115.8 million, down 7.7% year on year. This result surpassed analysts’ expectations by 0.9%. Overall, it was a strong quarter as it also logged a solid beat of analysts’ EPS estimates.

The stock is down 3.4% since reporting and currently trades at $64.22.

Read our full, actionable report on Power Integrations here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September, a quarter in November) have kept 2024 stock markets frothy, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there's still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.